Factors Affecting Personal Loan Eligibility: Complete Checklist

Anita wanted a personal loan to pay for an urgent medical expense. She had a regular income, so she expected the application to move ahead without any problems. During the process, the lender checked several details apart from her salary.

A regular income alone does not decide whether your loan gets approved. Lenders look at different factors before making a decision. This guide explains what they check and how you can improve your chances of getting a personal loan.

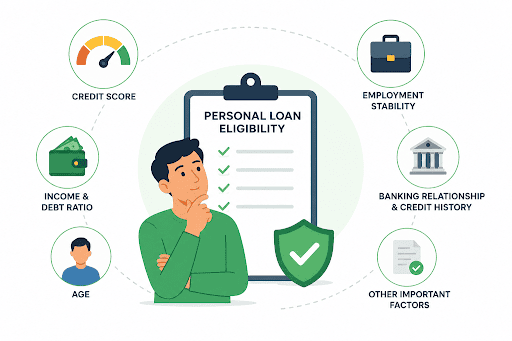

What Factors Affect Your Personal Loan Eligibility?

Lenders look at a few important things before approving a personal loan, so knowing the key Personal Loan Eligibility criteria can help you prepare better.

1. Credit Score: The Most Important Eligibility Factor

Your credit score shows how you have managed your loans and credit cards over the years. If you pay your EMIs and credit card bills on time, your score is likely to be better.

A good credit score gives lenders more confidence to approve your loan. If your score is low, they may offer a smaller loan, charge a higher interest rate, or may not approve your application.

2. Monthly Income and Debt-to-Income Ratio

Your monthly income helps lenders understand whether you can repay the loan comfortably. A stable income also shows that you can manage regular EMI payments without putting too much pressure on your finances.

Lenders also look at your debt-to-income ratio. This compares your monthly loan repayments with your monthly income. If a large part of your income already goes towards existing EMIs, getting another loan may become difficult.

3. Age: Eligibility Age Range for Personal Loans

Your age also affects your loan eligibility. Most lenders have a minimum and maximum age limit for personal loan applicants.

People with stable earnings years ahead often have a better chance of getting approved. Meeting the age requirements also gives lenders more confidence about timely repayments.

4. Employment Status and Job Stability

Lenders prefer borrowers with a stable source of income. They want to know that you can continue paying your EMIs throughout the loan tenure.

If you have worked with the same employer for a reasonable period or have a stable business income, your application may receive a stronger assessment.

5. Banking Relationship and Credit History

A long banking relationship can work in your favor. If you have maintained your account well and used banking services responsibly, lenders already have a better understanding of your financial habits.

Your credit history also plays an important role. Paying loans and credit card bills on time builds trust and improves your chances of approval.

6. Additional Factors Affecting Loan Eligibility

Apart from the major factors, lenders also review a few additional details before making a decision.

Residence Status and Address Stability

A stable residential address helps lenders verify your details quickly. Frequent address changes may require additional verification.

Existing Loan Obligations and EMIs

Lenders review your existing loans before approving a new one. Lower EMI commitments usually improve your repayment capacity.

Financial Documents and Verification

You should keep your original documents handy for the lenders to verify. This helps in faster approvals without any delays.

Co-Applicant Support

A co-applicant with a stable income and a good credit profile may improve your chances of getting a loan. This can be useful if your individual eligibility falls short.

How to Improve Your Personal Loan Eligibility?

Getting rejected once does not mean you cannot qualify later. A few simple financial habits can improve your profile and increase your chances of getting a personal loan.

Increase Your Credit Score

Lenders offer easy loans to people with high credit scores, as the risk level is very low. You can increase your credit score by paying your EMIs on time and avoiding missed payments.

Decrease Your Debt-to-Income Ratio

If you already have small loans or outstanding credit balances, getting a new loan becomes more difficult. Ensure you pay off those small loans to reduce your monthly EMIs.

Build Employment Stability

A steady job gives lenders more confidence. If you plan to apply for a personal loan, avoid changing jobs unless it is necessary.

Maintain a Healthy Banking Relationship

Use your bank account for your regular transactions and avoid leaving it inactive. A well-managed account can support your loan application.

Organize Financial Documents

Keep your salary slips, bank statements, identity proof, address proof, and other required documents ready. Complete documents can speed up the verification process and reduce delays.

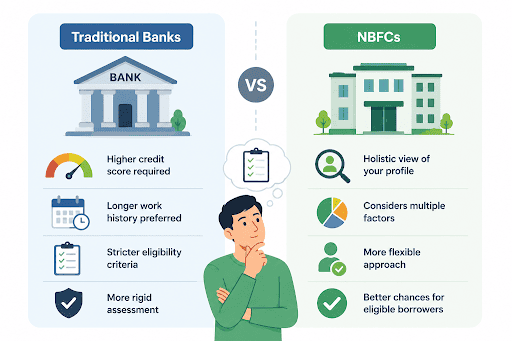

Personal Loan Eligibility: NBFC vs Traditional Banks

Banks and NBFCs check many of the same details before approving a personal loan. Banks may ask for a stronger credit score or a longer work history before they approve an application.

NBFCs may look at your financial situation more broadly instead of focusing on just one requirement. This can help borrowers with a regular income who may not qualify under a bank's lending criteria.

Hero FinCorp Personal Loan Eligibility: Flexible Assessment

Every borrower's financial situation is different. Instead of focusing on a single factor, Hero FinCorp considers multiple factors when assessing personal loan applications. This helps many eligible borrowers access funds more easily.

If you are planning to apply for a personal loan, Hero FinCorp offers a simple online application process with clear eligibility requirements. You can use the personal loan app to check your eligibility and apply online in just a few steps.

Frequently Asked Questions

Does self-employment affect personal loan eligibility?

No. Self-employed individuals can also get a personal loan if they meet the lender's eligibility requirements.

How does credit history impact loan eligibility?

A good credit history shows that you have repaid your loans on time. This can improve your chances of getting a personal loan.

Can I improve my eligibility before applying for a loan?

Yes. Improving your credit score, reducing existing EMIs, and maintaining a stable income can strengthen your loan application.

Are there different eligibility criteria for different loan amounts?

Yes. Lenders may review additional details when you apply for a higher loan amount because the repayment risk also increases.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.